Alberta’s tax advantage—not what it used to be

Up until last year, Alberta had an unambiguous tax advantage over every Canadian province and most U.S. states (particularly on personal income tax rates). Fast forward to today. With increases to personal, corporate, excise and carbon taxes, Alberta’s tax advantage in several categories has diminished or disappeared.

Alberta isn’t just losing ground with rival U.S. energy jurisdictions such as Texas and North Dakota that have low (or no) state-level personal and corporate taxes, but against its two neighbouring provinces.

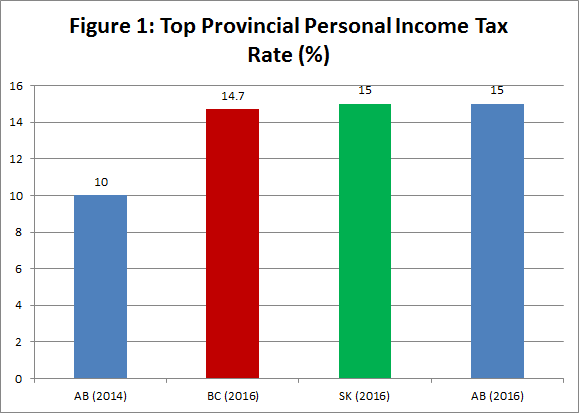

The chart below shows that Alberta’s top personal income tax rate in 2014 under the single 10 per cent tax rate was indeed much lower than the current top marginal rates in British Columbia and Saskatchewan. Following the change last year, the new top personal income tax rate in Alberta is tied with Saskatchewan at 15 per cent. B.C. reduced its top rate of 16.8 per cent this year to 14.7 per cent, so it’s now slightly below the top marginal tax rate in Alberta and Saskatchewan.

Of course, the top statutory marginal tax rate isn't the only important determinant of a jurisdiction's personal income tax competitiveness. The thresholds at which various rates apply, and overall effective tax rates at various levels of income, are also important. However, the top marginal tax rate is an important measure of competitiveness, especially given their important impact on marginal work and investment decisions for high earners. For these reasons, Alberta's loss of its tax advantage with respect to top marginal income tax rates compared to neighbouring jurisdictions represents the loss of an important competitive advantage.

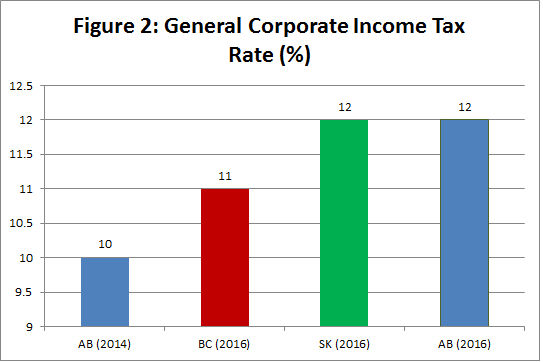

The second chart below tells a similar story when it comes to corporate taxes. In 2014, Alberta’s general corporate income tax rate was indeed below the rates in Saskatchewan and B.C. After the 20 per cent increase in the rate last year, Alberta leapfrogged B.C. and is now tied with Saskatchewan.

The loss of Alberta’s tax advantage with respect to personal and corporate income tax rates is particularly troubling since these are among the most economically inefficient taxes governments in Canada impose. This means that they cause more economic damage for each dollar of government revenue raised than most other types of taxes. Competitive personal and corporate income tax rates were therefore an important advantage that Alberta very recently enjoyed over its neighbours and several other jurisdictions, and the loss of that advantage is a blow to the province’s economic environment.

Alberta’s tax advantage with respect to corporate and personal income taxes has helped drive economic growth in the province for years. The loss of these tax advantages has unfortunately undermined Alberta’s competitiveness relative to key jurisdictions in Canada and the United States. Focusing on tax competitiveness and rebuilding the province's tax advantage would help Alberta remain a magnet for talent and investment. Lately, however, the province has been moving in the wrong direction.

Authors:

Subscribe to the Fraser Institute

Get the latest news from the Fraser Institute on the latest research studies, news and events.