Alberta budget should target personal income taxes

The Kenney government, which tables its first budget next week, inherited a fiscal mess in Alberta largely caused by spending increases by successive governments of varying party stripes. As a result, the government’s prospective plans to balance the budget are getting a lot of deserved attention. But while balancing the budget is important, so is tax competitiveness. Tax cuts generally reduce government revenue, but at least in the short term, reducing Alberta’s uncompetitive top personal income tax rate shouldn’t necessarily wait until the budget is balanced.

Alberta has long been thought of as a low-tax jurisdiction, in part due to the lack of a sales tax. But more importantly, the provincial government had low personal and corporate income tax rates ever since the Klein-era rate reductions. In fact, as of 2014, the province had both the lowest combined (state/provincial/federal) top personal income tax rate and general corporate income tax rate in either Canada or the United States. Much has changed since then, and not for the better.

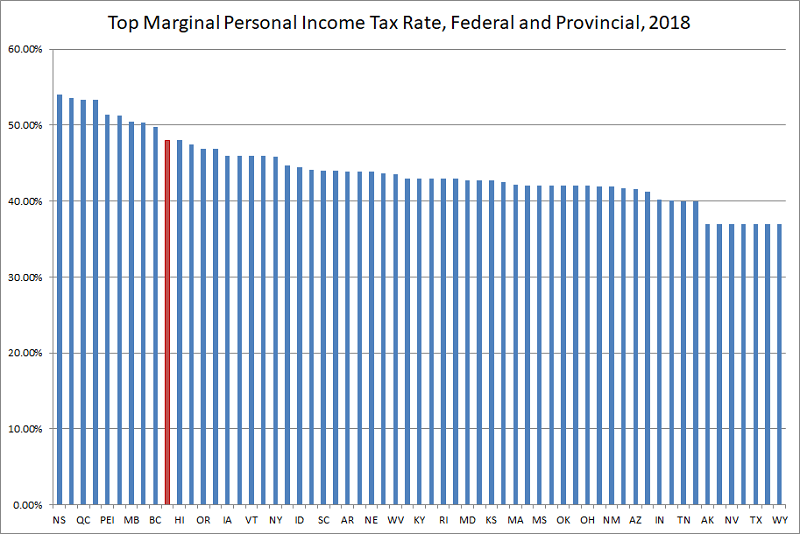

Since 2014, the Government of Alberta increased its top personal income tax rate from 10 per cent to 15 per cent while the federal government raised its top rate to 33 per cent. As a result, the top combined personal income tax rate in Alberta is now 48 per cent compared to 39 per cent in 2014. Meanwhile, the U.S. dropped its top federal personal income tax rate to 37 per cent, and several states don’t have a state level PIT at all. The net result of these changes can be seen below.

While Alberta had the lowest top personal income tax rate of any state or province in 2014, by 2018 it had the tenth highest top rate. And American tax filers can earn more than twice as much as Albertans before hitting the top bracket. Given the importance of attracting top talent to Alberta, having a top personal income tax rate 11 percentage points higher than, for instance, Texas is problematic.

To its credit, this provincial government has already tackled corporate income taxes by announcing a gradual four percentage-point reduction over a four-year period. But it should also make room for personal income tax reform. According to our calculations, both personal and corporate income tax reform could be implemented while balancing the budget over a three-year period with a 10.9 per cent nominal reduction in program spending. This approach to government spending would also make room for further pro-growth tax reform such as removing capital gains from provincial income taxes.

To provide a bit of historical context, a 10.9 per cent nominal spending reduction would be about half as large as the 20 per cent nominal reduction of the Klein era. It would also bring Alberta much closer into line with other large provinces—British Columbia, for example, now spends about 20 per cent less per person than Alberta.

While balancing the budget is a priority, personal income tax reform and relief should be as well. Fortunately, these two goals are not mutually exclusive. And both should be done in short order.

Author:

Subscribe to the Fraser Institute

Get the latest news from the Fraser Institute on the latest research studies, news and events.